It’s been a wild experience for the inventory markets this 12 months, and the wildest of all of them was the trail of development shares. Shares that surged lots of of share factors, with traders chasing after them, ready to pay virtually any value – crashed spectacularly, shedding all their glamor. These beforehand attractive and thrilling firms crumbled when the financial system and inventory market weakened, with a few of them shedding their mojo months earlier than the final markets went crashing down.

Extra Weekend Version Items:

Palantir’s Bullish Case Stays Compelling after Large Drop

Listed here are 2 Shares to Think about for a Rebound

From Heroes to Zeroes: These 2 Shares Can Comeback

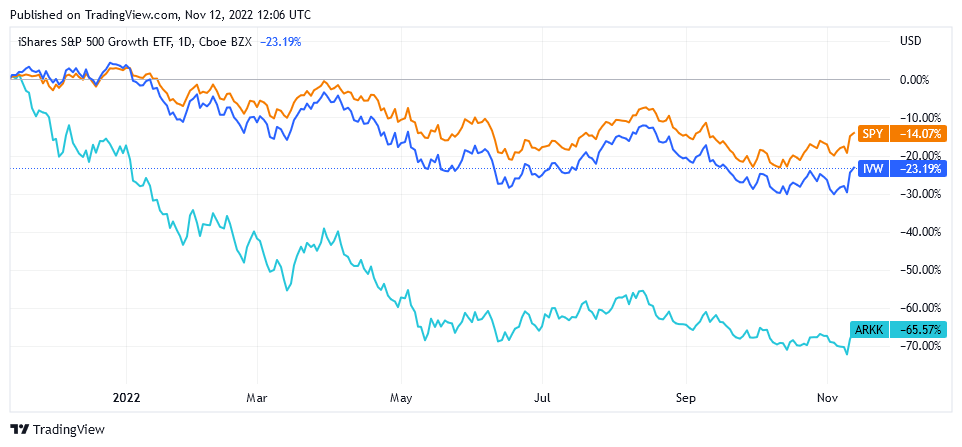

Many tech shares, large and small, have been hammered a lot over the past 12 months that traders are questioning if it is a repeat of the dot-com bust of the early 2000s. To inform the reality, there are fairly a number of similarities, with essentially the most placing being the loopy valuations of the tech shares which have now been virtually fully worn out.

From Progress to Bubble

These had been principally shares outdoors of Large Tech. Though the large-cap tech shares reached fairly excessive P/Es of 40x to 50x, these weren’t fully unfeasible contemplating that these are very worthwhile firms with wealthy money flows and helpful market shares – companies that registered excessive earnings development through the 2020-2021 rally. In fact, because the Fed turned course and operational and financing prices began rising, the valuations of Large Tech shares mirrored the unfavourable anticipated change in internet revenue; however the path of the massive caps is nothing just like a bubble and burst.

The shares of smaller, rapidly-growing firms had been a really completely different story: they had been buying and selling at price-to-sales ratios of above 30x (P/Es weren’t relevant right here as they had been principally unprofitable). These ratios steered they had been firmly in bubble territory, as nobody actually believed they might be capable of develop their gross sales as a lot as to deliver them in step with costs. Actually, the bubble was so apparent that many of those shares peaked months earlier than the Fed’s tightening pivot in November 2021.

Zoom Video (NASDAQ: ZM), Peloton (NASDAQ: PTON), Carvana (NYSE: CVNA), Fiverr (NYSE: FVRR), Shopify (NYSE: SHOP), and others had been the pandemic darlings, as, throughout lockdowns, life continued principally on-line. Peloton surged 725% from the pandemic’s low in March to its peak in December 2021 after which misplaced 95% of its worth, buying and selling at a a lot lower cost than earlier than the rally. One other lockdown darling, Zoom, rose 780% as much as its excessive in October 2021, then crashed by about 85%. Carvana rose 1,049% from March 2020 to August 2021, solely to drop like a rock by 97%, wiping out all of its positive factors and extra. Fiverr had rallied 1,126% to its peak in February 2021 earlier than it collapsed 91% to its pre-pandemic value of $27. These are just some examples out of oh so many.

What’s attention-grabbing is that these aren’t meme shares operating on hype solely however shares of firms promoting services and products that folks really like and purchase, even when a few of them misplaced some market share that was gained throughout lockdowns. Most of the firms that are actually on the verge of changing into penny shares are literally doing fairly properly, slicing prices and holding onto their revenues.

How Did They Fly So Excessive?

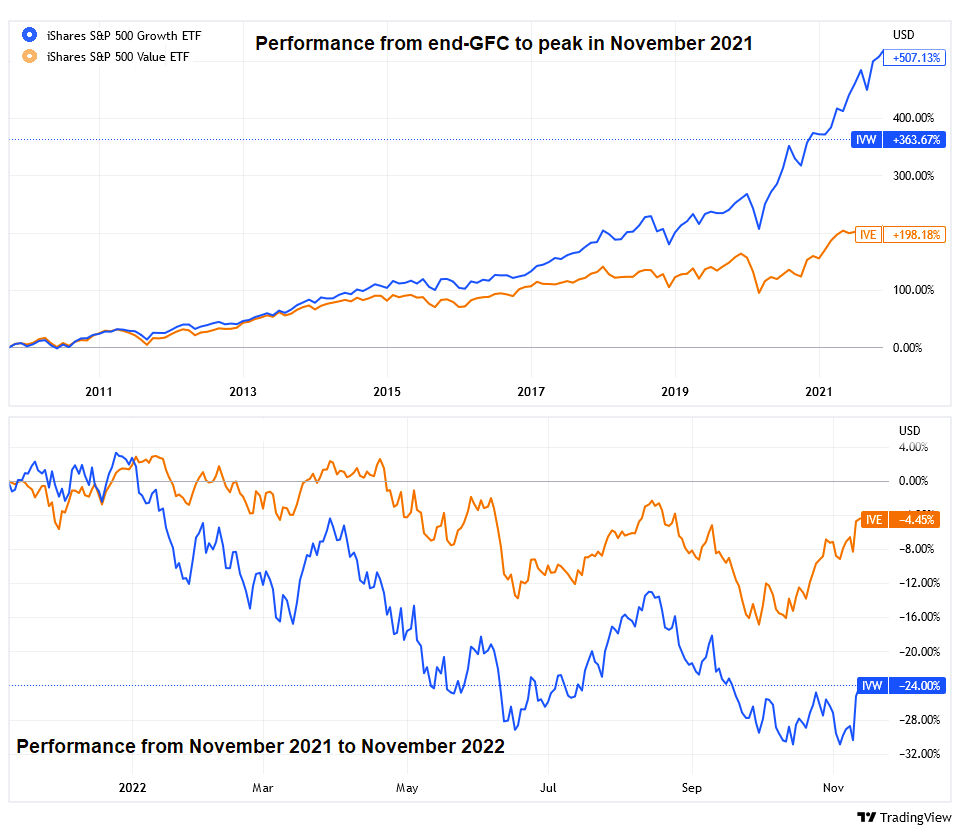

The widespread denominator for these shares, aside from their spectacular surge and much more spectacular downfall – is that they’re all thought of development shares. As customary for development shares, most of those firms are unprofitable however could have the potential to ship above-average returns over a long-term horizon because of investing within the improvement of revolutionary merchandise, companies, or enterprise fashions. The years after the International Monetary Disaster (GFC), with low rates of interest, low inflation, a bouncy financial system, and rising affection for all issues revolutionary, had been nice for development – however the COVID-19 pandemic, with all its hardships, was even higher.

{kind=link}

On the onset of the pandemic, the Federal Reserve took extraordinary measures to help monetary markets, slicing rates of interest to zero and injecting lots of of billions of {dollars} into the monetary system. The U.S. Congress did its half as properly, pumping trillions of {dollars} into the financial system by the use of prolonged unemployment advantages and stimulus checks. With bond yields at historic minimums and financial savings applications yielding zilch, all this cash had nowhere to go however the inventory markets.

In the meantime, falling and/or extra-low rate of interest surroundings favored development shares, whose future cash-flows had been abruptly discounted by a lot, a lot decrease charges whereas making the capital wanted for future growth dust low cost.

Earnings Do Matter

It’s common data that “the inventory market will not be the financial system.” That’s, the route of the inventory market doesn’t all the time replicate what’s occurring on Primary Road. Nonetheless, there may be one piece of the financial system that Wall Road is obsessed about – properly, aside from the occasions when mania du jour takes over: company income, notably the outlook for income over an extended horizon. In occasions like now, when the rates of interest are anticipated to rise till the financial system falls into recession after which some extra – these future income aren’t value a lot as we speak. When liquidity is scarce, nobody of their proper thoughts can pay an outrageous value for a inventory in an organization which will, or could not, flip in a revenue in a number of years – if the celebs align.

All isn’t over for development; the tide will flip, and they’re going to seemingly take over finally. In spite of everything, we live in a technology-driven, technology-focused, and technology-obsessed civilization; if not for the entrepreneurs with shiny concepts and the traders prepared to provide them a hand, we’d nonetheless be driving horse carriages, at greatest. So, in the long term, Tech will prevail. In the meantime, it’s in hassle. Nicely, not in hassle per se: the technological progress and the innovation received’t cease – however non-profitable high-maintenance development shares absolutely are.

Many traders are actually on the lookout for bargains within the inventory market, particularly among the many former high-fliers whose valuations have come right down to earth. The issue is that for a lot of merchants, “doing analysis” on a inventory means checking its value versus historical past. After they see that the inventory, whose value was at lots of of {dollars}, is now promoting for a couple of dollars, they consider that they’ve discovered an awesome entry level. Nonetheless, the value alone is usually a very deceptive indicator at its highs in addition to at its lows.

Beware the Entice

These wanting on the value solely are prone to falling right into a “worth entice” when their cheaply purchased holdings really by no means rebound as a result of they had been low cost for a purpose. In fact, the low value and low multiples could also be brought on solely by unfavourable investor sentiment. Alternatively, they might imply the corporate is experiencing monetary instability and has little development potential, and the inventory could proceed to languish or drop additional. To keep away from the entice, it’s advisable to try to uncover all of the “why’s” of the inventory habits, together with researching fundamentals and analyzing enterprise prospects.

For instance, Twilio (NYSE: TWLO) could also be value after the large value crash. Though Twilio’s internet revenue is unfavourable and anticipated to be unfavourable for some time extra, its buyer base and income are rising properly, it has rather more money than its whole debt (which can be very low vs. its belongings), and it has adequate money runway for greater than three years based mostly on its present free money move. As such, Twilio seems to be like a strong cut price for a longer-term funding.

One other potential “Purchase” could be the Israeli-born Fiverr. The inventory has already jumped greater than 40% from its low, however contemplating how low that low was, it’s nonetheless very, very low cost. What brought on the surge was spectacular Q3 outcomes, with revenues and earnings beating estimates by a large margin. Fiverr’s monetary place seems to be good, as its short-term belongings exceed its short- and long-term liabilities, it has additional cash than its whole debt, and it has adequate money runway for greater than three years as a result of free money move being constructive and rising. Fiverr’s inventory isn’t immune from the market’s gyrations, in fact, but it surely does seem like a probably worthwhile long-term funding.